New Financial World Order

‘Puter was reading this post regarding the failed HAMP program over at Megan McArdle’s blog at The Atlantic this morning, and it set him to thinking. Flawed notions of consumer credit are what dragged us in to our current straits, and flawed notions of consumer credit are prolonging our stay here. ‘Puter has after much thought come to the following conclusion:

‘Puter was reading this post regarding the failed HAMP program over at Megan McArdle’s blog at The Atlantic this morning, and it set him to thinking. Flawed notions of consumer credit are what dragged us in to our current straits, and flawed notions of consumer credit are prolonging our stay here. ‘Puter has after much thought come to the following conclusion:

America erroneously believed it could have the following three items simultaeously: (1) pre-meltdown style easy consumer credit; (2) solvent financial institutions; and (3) a strong economy. This belief caused the meltdown, and our refusal to reexamine this belief has prolonged the downturn. We are now faced with the stark truth. We can only have (2) and (3) to the exclusion of (1). Grown up Americans are now faced with a binary choice. Which shall we have, a federally enforced entitlement to easy consumer credit or a financially stable nation? ‘Puter chooses financial stability over easy credit every day of the week.

But back to HAMP. HAMP is a natural policy outgrowth of the belief that we can have (1), (2) and (3) simultaneously. HAMP is premised on the idea that given enough time, surely homeowners who never should have received loans in the first place will magically discover the ability to repay their debts. The always-just-over-the-horizon economic recovery will surely rescue us. What the Obama Administration either fails to see or cynically ignores for populist reasons is that perpetuating easy consumer credit prevents any meaningful recovery. The policies touted as helping Americans actually forestall the promised relief.

If we are to see recovery, we will necessarily see a contraction in consumer credit. That is not to say less money will be available. It is to say that money will be available to fewer people. In order to permit the credit contraction to operate properly, ushering in an economic recovery, we must remove the government installed roadblocks to orderly liquidation of debts and collateral assets.

‘Puter could go on forever about the insidious cancer of market-deforming government programs. Fannie Mae, Freddie Mac and the FHA are prime examples. The Community Reinvestment Act and the Small Business Administration are also flagrant offenders. ‘Puter’s certain each of you have your own favorite examples. The common thread among each of these is government subsidization of an otherwise risky, uneconomic relationship. In short, banks would not lend to many of these people and businesses were it not for the fact that the government pledged taxpayer monies to guarantee the foolish loans. If you look at the securitized debt that caused our trouble, each bond issue contained significant numbers of uneconomic loans that were improperly valued as a result of the implicit federal guarantee of payment. The sooner government gets out of the business of telling business how to do business, the sooner the economy will recover.

To be certain, in an orderly liquidation individuals will be hurt. People will lose their homes and their businesses. Banks will take hits to their balance sheets as they realize losses. Stockholders will suffer as their holdings in financial institutions fall to realistic values. Please note carefully that the government still plays a critical role in this process: it must ensure the liquidation is orderly. ‘Puter is not a fan of TARP, but neither can he prove that it was not necessary. TARP was intended to temporarily prop up financial institutions so that there could be an orderly liquidation, and it appears to have done so. Bankruptcy also provides a time-tested and accepted methodology for orderly liquidation. ‘Puter does not intend to diminish the coming painful times, he simply notes that the pain is necessary to ensure recovery.

And what will a future after liquidation and return to normalcy look like? ‘Puter’s guessing that the lending environment will tighter all around. Business will have access to capital and will be lending, but rates will be higher, even for the best businesses. Banks will actually enforce financial covenants this time around, at least until this mess is forgotten. Durations will be shorter, borrowing documents tighter. Banks will still take risk, but they will better evaluate the risk and charge borrowers a commensurate risk premium. Commercial borrowers unable to borrower through traditional means will be able to borrow through venture capitalists or other private funding, but they will pay for the privilege. We may even see a return to equity issues rather than debt issues. The times are changing.

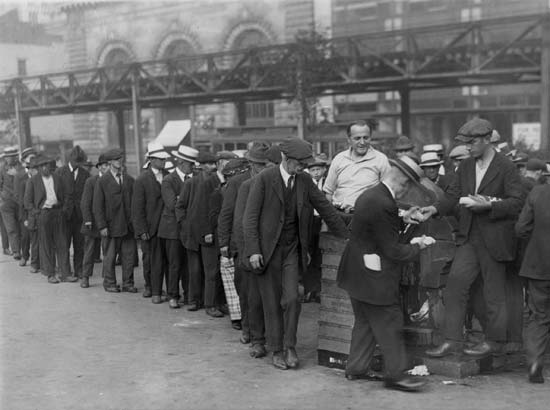

Consumers will have it even tougher. It will be more difficult to get mortgages, to say nothing of unsecured credit. Gone are the days of sub-650 scored consumers receiving multiple credit card offers. These people will be fortunate to have any access to credit at affordable rates. Home ownership rates will drop. College attendance will drop, or college prices will drop, and probably some combination of the two. ‘Puter believes that America will see a growing gap in standard of living between the top 50% and the bottom 50%. The bottom 50%’s easy credit fueled spending spree allowed it to close the gap from the late 1980s to today, but that credit’s now gone. These folks will not be able to keep up with the Jones. Smaller houses or rented apartments, 10 year old used cars, second hand furniture, last generation TVs, no-cations in lieu of stay-cations, it’s all coming to a community near you.

And as the standard of living falls, we will see a large class of lower to middle income people rise. They will be roughly defined as those who have seen their standard of living fall. And they will be angry, seemingly cheated out of their American Dream, and looking for someone to blame.

What does this portend for America’s future? ‘Puter’s not certain, but it certainly isn’t going to be fun to live through.

Always right, unless he isn’t, the infallible Ghettoputer F. X. Gormogons claims to be an in-law of the Volgi, although no one really believes this.

’Puter carefully follows economic and financial trends, legal affairs, and serves as the Gormogons’ financial and legal advisor. He successfully defended us against a lawsuit from a liquor distributor worth hundreds of thousands of dollars in unpaid deliveries of bootleg shandies.

The Geep has an IQ so high it is untestable and attempts to measure it have resulted in dangerously unstable results as well as injuries to researchers. Coincidentally, he publishes intelligence tests as a side gig.

His sarcasm is so highly developed it borders on the psychic, and he is often able to insult a person even before meeting them. ’Puter enjoys hunting small game with 000 slugs and punt guns, correcting homilies in real time at Mass, and undermining unions. ’Puter likes to wear a hockey mask and carry an axe into public campgrounds, where he bursts into people’s tents and screams. As you might expect, he has been shot several times but remains completely undeterred.

He assures us that his obsessive fawning over news stories involving women teachers sleeping with young students is not Freudian in any way, although he admits something similar once happened to him. Uniquely, ’Puter is unable to speak, read, or write Russian, but he is able to sing it fluently.

Geep joined the order in the mid-1980s. He arrived at the Castle door with dozens of steamer trunks and an inarticulate hissing creature of astonishingly low intelligence he calls “Sleestak.” Ghettoputer appears to make his wishes known to Sleestak, although no one is sure whether this is the result of complex sign language, expert body posture reading, or simply beating Sleestak with a rubber mallet.

‘Puter suggests the Czar suck it.